Productivity: More with Less by Better

Available resources are scarce. To sustain our society's income and living standards in a world with ecological and demographic change, we need to make smarter use of them.

Dossier

In a nutshell

Nobel Prize winners Paul Samuelson and William Nordhaus state in their classic economics textbook: Economics matters because resources are scarce. Indeed, productivity research is at the very heart of economics as it describes the efficiency with which these scarce resources are transformed into goods and services and, hence, into social wealth. If the consumption of resources is to be reduced, e. g., due to ecological reasons, our society’s present material living standards can only be maintained by productivity growth. The aging of our society and the induced scarcity of labour is a major future challenge. Without productivity growth a solution is hard to imagine. To understand the processes triggering productivity growth, a look at micro data on the level of individual firms or establishments is indispensable.

Our experts

Department Head

If you have any further questions please contact me.

+49 345 7753-708 Request per E-Mail

President

If you have any further questions please contact me.

+49 345 7753-700 Request per E-MailAll experts, press releases, publications and events on “Productivity”

Productivity is output in relation to input. While the concept of total factor productivity describes how efficiently labour, machinery, and all combined inputs are used, labour productivity describes value added (Gross Domestic Product, GDP) per worker and measures, in a macroeconomic sense, income per worker.

Productivity Growth on the Slowdown

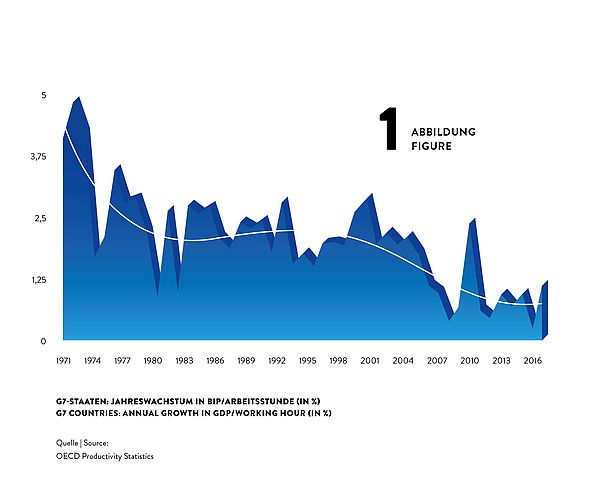

Surprisingly, despite of massive use of technology and rushing digitisation, advances in productivity have been slowing down during the last decades. Labour productivity growth used to be much higher in the 1960s and 1970s than it is now. For the G7 countries, for example, annual growth rates of GDP per hour worked declined from about 4% in the early 1970s to about 2% in the 1980s and 1990s and then even fell to about 1% after 2010 (see figure 1).

This implies a dramatic loss in potential income: Would the 4% productivity growth have been sustained over the four and a half decades from 1972 to 2017, G7 countries’ GDP per hour would now be unimaginable 2.5 times as high as it actually is. What a potential to, for instance, reduce poverty or to fund research on fundamentals topics as curing cancer or using fusion power!

So why has productivity growth declined dramatically although at the same time we see, for instance, a boom in new digital technologies that can be expected to increase productivity growth? For sure, part of the decline might be spurious and caused by mismeasurement of the contributions of digital technologies. For instance, it is inherently difficult to measure the value of a google search or another video on youtube. That being said, most observers agree that part of the slowdown is real.

Techno-Pessimists and Techno-Optimists

Techno-pessimists say, well, these new technologies are just not as consequential for productivity as, for instance, electrification or combustion engines have been. Techno-optimists argue that it can take many years until productivity effects of new technologies kick in, and it can come in multiple waves. New technology we have now may just be the tools to invent even more consequential innovations in the future.

While this strand of the discussion is concerned with the type of technology invented, others see the problem in that inventions nowadays may diffuse slowly from technological leaders to laggards creating a wedge between few superstar firms and the crowd (Akcigit et al., 2021). Increased market concentration and market power by superstar firms may reduce competitive pressure and the incentives to innovate.

Finally, reduced Schumpeterian business dynamism, i.e. a reduction in firm entry and exit as well as firm growth and decline, reflects a slowdown in the speed with which production factors are recombined to find their most productive match.

While the explanation for and the way out of the productivity puzzle are still unknown, it seems understood that using granular firm level data is the most promising path to find answers.

What are the Origins of Productivity Growth?

Aggregate productivity growth can originate from (i) a more efficient use of available inputs at the firm level as described above or (ii) from an improved allocation of resources between firms.

Higher efficiency at the firm level captures, e.g., the impact of innovations (Acemoglu et al., 2018) or improved firm organisation (management) (Heinz et al., 2020; Müller und Stegmaier, 2017), while improved factor allocation describes the degree of which scarce input factors are re-allocated from inefficient to efficient firms (‘Schumpeterian creative destruction’) (Aghion et al., 2015; Decker et al., 2021).

Most economic processes influence the productivity of existing firms and the growth and the use of resources of these firms and their competitors as well. The accelerated implementation of robotics in German plants (Deng et al., 2020), the foreign trade shocks induced by the rise of the Chinese economy (Bräuer et al., 2019), but also the COVID-19 pandemic, whose consequences are still to evaluate (Müller, 2021) not only effects on productivity and growth of the firms directly affected but at the same time may create new businesses and question existing firms.

While productivity can be measured at the level of aggregated sectors or economies, micro data on the level of individual firms or establishments are indispensable to study firm organisation, technology and innovation diffusion, superstar firms, market power, factor allocation and Schumpeterian business dynamism. The IWH adopts this micro approach within the EU Horizon 2020 project MICROPROD as well as with the CompNet research network.

As “creative destruction” may also negatively affect the persons involved (e. g., in the case of layoffs, Fackler et al., 2021), the IWH analyses the consequences of bankruptcies in its Bankruptcy Research Unit and looks at the implications of creative destruction for the society, e. g., within a project funded by Volkswagen Foundation searching for the economic origins of populism and in the framework of the Institute for Research on Social Cohesion.

Publications on “Productivity”

On the International Dissemination of Technology News Shocks

in: IWH Discussion Papers, No. 25, 2020

Abstract

This paper investigates the propagation of technology news shocks within and across industrialised economies. We construct quarterly utilisation-adjusted total factor productivity (TFP) for thirteen OECD countries. Based on country-specific structural vector autoregressions (VARs), we document that (i) the identified technology news shocks induce a quite homogeneous response pattern of key macroeconomic variables in each country; and (ii) the identified technology news shock processes display a significant degree of correlation across several countries. Contrary to conventional wisdom, we find that the US are only one of many different sources of technological innovations diffusing across advanced economies. Technology news propagate through the endogenous reaction of monetary policy and via trade-related variables. That is, our results imply that financial markets and trade are key channels for the dissemination of technology.

Decentralisation of Collective Bargaining: A Path to Productivity?

in: IWH-CompNet Discussion Papers, No. 3, 2020

Abstract

Productivity developments have been rather divergent across EU countries and particularly between Central Eastern Europe (CEE) and elsewhere in the continent (non-CEE). How is such phenomenon related to wage bargaining institutions? Starting from the Great Financial Crisis (GFC) shock, we analyse whether the specific set-up of wage bargaining prevailing in non-CEE may have helped their respective firms to sustain productivity in the aftermath of the crisis. To tackle the issue, we merge the CompNet dataset – of firm-level based productivity indicators – with the Wage Dynamics Network (WDN) survey on wage bargaining institutions. We show that there is a substantial difference in the institutional set-up between the two above groups of countries. First, in CEE countries the bulk of the wage bargaining (some 60%) takes place outside collective bargaining schemes. Second, when a collective bargaining system is adopted in CEE countries, it is prevalently in the form of firm-level bargaining (i. e. the strongest form of decentralisation), while in non-CEE countries is mostly subject to multi-level bargaining (i. e. an intermediate regime, only moderately decentralised). On productivity impacts, we show that firms’ TFP in the non-CEE region appears to have benefitted from the chosen form of decentralisation, while no such effects are detectable in CEE countries. On the channels of transmission, we show that decentralisation in non-CEE countries is also negatively correlated with dismissals and with unit labour costs, suggesting that such collective bargaining structure may have helped to better match workers with firms’ needs.

Measuring the Indirect Effects of Adverse Employer Behaviour on Worker Productivity – A Field Experiment

in: Economic Journal, No. 632, 2020

Abstract

We conduct a field experiment to study how worker productivity is affected if employers act adversely towards their co-workers. Our employees work for two shifts in a call centre. In our main treatment, we lay off some workers before the second shift. Compared to two control treatments, we find that the lay-off reduces the productivity of unaffected workers by 12%. We find suggestive evidence that this result is not driven by altered beliefs about the job or the management’s competence, but caused by the workers’ perception of unfair employer behaviour. The latter interpretation is confirmed in a prediction experiment with professional HR managers. Our results suggest that the price for adverse employer behaviour goes well beyond the potential tit for tat of directly affected workers.

Promoting Higher Productivity in China — Does Innovation Expenditure Really Matter?

in: Singapore Economic Review, No. 5, 2020

Abstract

The slowing down of the global economy adds additional challenges to China? economic policies as the country orchestrates its transition to lower resource dependency and higher technology intensity of output. Are policies aimed at technologically advanced sectors the right answer? Drawing from a newly created dataset of firms? balance sheets over the period 1998?2013, matched with patents data until 2009, we uncover that expenditure in innovation had limited effect on boosting productivity, without generating a clear gain in overall productivity for the high-tech sector. As a matter of fact, there is a much higher dispersion in productivity outcomes in firms belonging to the low-technology sectors, which derives from a bunch of champions in those sectors scoring higher productivity dynamics than in the High-technology sectors. The paper finds those barriers to entry and in general, market power of incumbents in the high-tech generate less than optimal resource reallocation, which hampers the overall productivity. Policies should presumably aim at removing such obstacles rather than solely promote innovation expenditure.

Special Issue on Productivity: Introduction

in: Singapore Economic Review, No. 5, 2020

Abstract

At the time we write this introduction, the world is entering a second phase of the COVID-pandemic, where all countries in the world attempt to gradually reopen after the tremendous shock on lives and economic activity. The focus of the policies right now is very much on short-term interventions aimed at alleviating the financial strains on households and firms, thus fostering a quicker recovery. In the medium and long-term perspective, however, it would be essential to parallel such policies with appropriate interventions aimed at strengthening the aggregate productivity of the economy, with the objective of increasing resilience and foster more solid growth foundations.