Communication instead of conflict – why are female CEOs so interesting for hedge funds

For the study, a sample of 42,831 U.S. firm data and 2,410 hedge fund activism events from 2003 to 2018 were analysed. During this period, the economic importance of activist hedge funds also increased significantly. While they managed $12 billion in the U.S. in 2003, by 2018 the figure had risen to more than $100 billion. For the survey, the researchers explored the following questions: Is there a systematic association between female CEOs and the probability of activist hedge funds targeting their firms, and if so, why? Do these investors approach female firm leaders differently than male firm leaders? Do female-led target firms perform differently after targeting compared to male-led target firms?

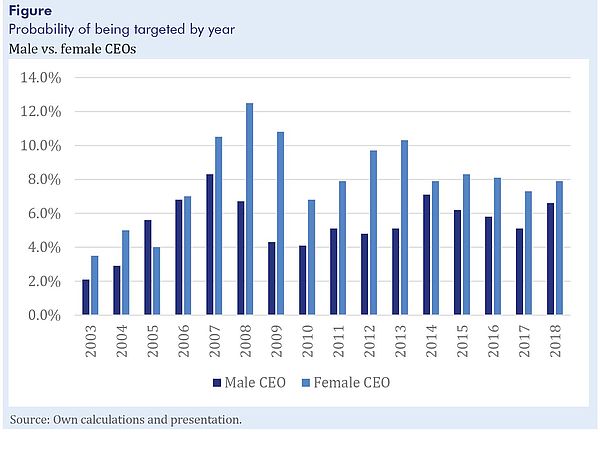

As the study also indicates, activist hedge funds target female-led firms more often. The likelihood of attracting the interest of an activist hedge fund is 52% higher for a firm with a female CEO (see figure). "This study doesn't just highlight gender differences, but also provides an indication of the link between soft skills and profitability," comments IWH President Reint Gropp. This is because activist hedge funds rely on communication and collaboration with CEOs: The average share of activist hedge funds in the firms they invest in is less than 9%, which is far from a controlling stake. The most common goal of hedge fund activism – almost half of all hedge fund activism events – is to increase shareholder value through communication with management. Only when the management does not want to cooperate with the activist investors the latter drive campaigns to bring other shareholders on board.

The transformational leadership style of female CEOs has a significant impact on how activism campaigns transform target firms and improve share price. Female CEOs are more likely to communicate and cooperate with hedge fund activists rather than attacking them. This lowers implementation costs and increases success rates. As a result, expected returns to the hedge fund increase. Possessing strong soft skills, female CEOs are more likely to accept hedge fund activists’ advice and expertise, thereby improving operational performance.

Male CEOs, on the other hand, tend to be more aggressive in negotiations, more self-centered and more power-oriented. Accordingly, they are more likely to resist hedge fund activists' suggestions, resulting in campaigns that are costly for both parties. Those campaigns reduce rather than increase the value of the firm. As the data show, female CEOs are significantly more likely to settle such power struggles than male business leaders. "This proves that communication and collaboration during activism campaigns are more likely with female CEOs," Hasan sais.

A counterfactual test confirms the result. If activist hedge funds' need for communication drops because they don't seek active participation, then the gender effect also disappears. To examine this possibility, they compared the applications of the U.S. Securities and Exchange Commission (SEC) for an acquisition of more than 5% of the shares. There are two groups in the U.S.: Schedule 13D and Schedule 13G. The latter can be applied for by investors if, among other things, they do not wish to become actively involved in the firm. There is no preference for female CEOs when activist hedge funds file 13G, where they act as quasi-passive investors in firms and therefore do not need to cooperate with firm management.

The study also analysed dynamic changes in target firms two years before and up to two years after hedge fund engagement. "After adjusting for industry and year effects, both female- and male-led target firms increase their operating profitability in the two years after entry, but the increase is significantly larger for female-led target firms," Gropp summarises. This finding is consistent with hedge fund activists' goals of increasing dividend payout and performance.

Publication

Bill Francis, Iftekhar Hasan, Yinjie (Victor) Shen, Qiang Wu: Do Activist Hedge Funds Target Female CEOs? The Role of CEO Gender in Hedge Fund Activism, in: Journal of Financial Economics, Vol. 141 (1), 2021, 372-393.

Whom to contact

For Researchers

President

If you have any further questions please contact me.

+49 345 7753-700 Request per E-MailFor Journalists

Head of Public Relations

If you have any further questions please contact me.

+49 345 7753-720 Request per E-MailIWH list of experts

The IWH list of experts provides an overview of IWH research topics and the researchers and scientists in these areas. The relevant experts for the topics listed there can be reached for questions as usual through the IWH Press Office.

Related Publications

Do Activist Hedge Funds Target Female CEOs? The Role of CEO Gender in Hedge Fund Activism

in: Journal of Financial Economics, 1, 2021

Abstract

Using a comprehensive US hedge fund activism dataset from 2003 to 2018, we find that activist hedge funds are about 52% more likely to target firms with female CEOs compared to firms with male CEOs. We find that firm fundamentals, the existence of a “glass cliff,” gender discrimination bias, and hedge fund activists’ inherent characteristics do not explain the observed gender effect. We also find that the transformational leadership style of female CEOs is a plausible explanation for this gender effect: instead of being self-defensive, female CEOs are more likely to communicate and cooperate with hedge fund activists to achieve intervention goals. Finally, we find that female-led targets experience greater increases in market and operational performance subsequent to hedge fund targeting.