German Economy: Strong domestic demand compensates for weak exports

The development on the German labour market is increasingly affected by the strong migration movements. The rise in migration is mainly caused by the free movement of workers from Central and Eastern European countries, the difficult labour market situation in the countries affected by the European debt and confidence crisis (Greece, Italy, Portugal, Spain) and the increased immigration of refugees. In 2015, the overall migration balance in Eastern Germany should be about 170 000 persons, 70% of which are from the main countries of origin of people seeking asylum (see figure).

Global Prospects

Notwithstanding high volatilities on the foreign exchange, capital and commodity markets, world production is expanding moderately and without strong fluctuations. The economies of the United States and the United Kingdom are on the upswing, while the euro area is recovering modestly. Economic activity in China seems to stabilise following a pronounced period of weakness at the beginning of 2015. The recessions in Brazil and Russia continue. Both commodity exporters are troubled by the sharp drop in prices for their commodities that has been caused by battles for market shares and by the continuing weakness of investment and manufacturing in China and elsewhere. Worldwide economic activity in the service sector proved resilient, on the other hand.

As a consequence of the decline in commodity prices, inflation rates are close to zero, as are the policy rates in many developed economies. Due to the economic upturn in the United States, however, the Federal Reserve is expected to raise its policy rate in December. The ECB and the Bank of Japan aim at providing the modest dynamics of their respective economies stimuli via a continuing broadening of the monetary base. Fiscal policy will be eased during 2016, turning expansive in the euro zone. Nonetheless, worldwide production is not expected to expand much stronger in 2016 compared to the current year. Worldwide demand is primarily backed by low interest rates and low prices for energy and commodities. However, these pose substantial risks for the stability of economies that are dependent on commodity export revenues. Overall, this forecast expects world production to increase by 2.6% in 2015, by 2.7% in 2016 and by 2.8% in 2017.

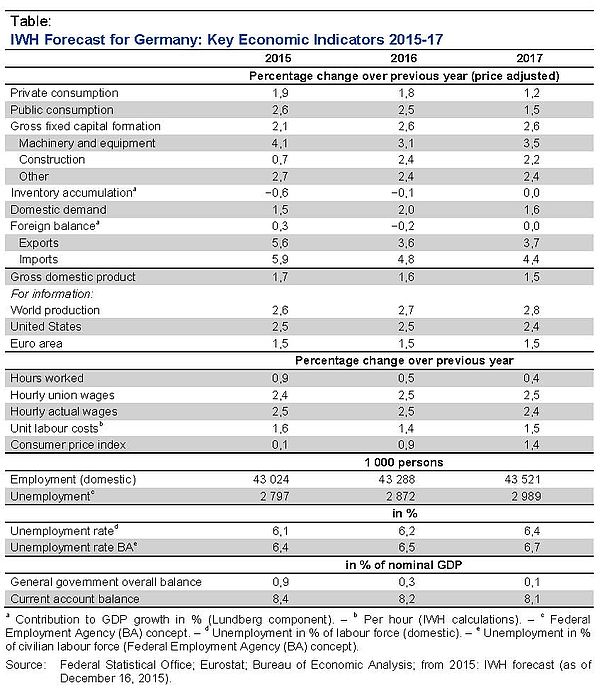

German Economic Perspectives

Economic activity in Germany is on a modest upswing. Most recently it has been backed by private consumption expenditures. The dynamics of exports have remarkably slowed down since the middle of the year. The weakness of emerging market economies curbed the external demand for German products. Gross fixed capital formation has decreased since the summer. Investment activities have been depressed by the partially remarkable under-utilisation in major industries. The German economy is expected to lose some further momentum in the final quarter of 2015.

At the beginning of the year 2016, economic activity will accelerate again, primarily due to continued favourable income prospects. These are favoured by positive dynamics on the labour market. Households’ purchasing power is further strengthened by the recent fall in energy prices. Hence, private consumption is further expected to notably contribute to GDP growth. Exports are backed by the weak euro, a continuous recovery within the euro area and an expected stabilisation of demand from emerging market economies. Against this background, corporate investment activities are supposed to increase, also fostered by favourable financing conditions. The stimulating effects of the exchange rate and the low energy prices are likely to expire in the course of the year 2016. Economic dynamics are expected to be slightly weaker in 2017.

Overall, this forecast expects German GDP to increase by 1.7% in 2015, by 1.6% in 2016 and by 1.5% in 2017. The fourth quarter year-on-year growth rate increases from a modest 1.3% in 2015 to 1.8% in the year 2016 and decreases to 1.6% in the year thereafter. Consumer price inflation increases slightly over the forecast horizon, also as a consequence of firms shifting higher wage costs due to the introduction of the minimum wage to consumers. The 66% forecast interval for GDP growth ranges from 1.6% to 1.8% in 2015, from 0.8% to 2.5% in 2016 and from −0.3% to 3.2% in the year 2017. Employment is expected to further increase over the forecast horizon, with the number of jobs subject to social insurance contributions continuing to increase stronger than total employment. The number of employed persons among the refugees will initially be low, as a consequence of tedious bureaucratic processes associated with applications for permits as well as insufficient language skills and often low levels of qualification. A large proportion of asylum seekers is therefore expected to initially become unemployed and to raise the registered number of unemployed persons.

On the Distribution of Refugees in the European Union

In order to meet the challenges of current forced migration EU member states should cooperate in the field of asylum policy more closely. In particular, it is recommendable distributing incoming refugees across member states using an allocation mechanism depending on differentials in national integration costs. An efficient distribution of refugees within the EU is achieved by balancing the incremental costs of integrating an additional refugee across member states. Thereby the allocation scheme should also take into account the positive effects of migration such as an increasing labour force potential in aging and shrinking societies. In general, however, the national financial capacity with respect to refugee integration does not automatically coincide with the integration capacity of the respective country. This is why a stable political agreement can only be achieved if the allocation mechanism is combined with an additional compensation scheme. This compensation scheme could consist of monetary side-payments to countries that have a low economic capacity relative to their national integration capacity (low incremental cost of integration, high migration benefits). In principle the allocation mechanism that has been recently proposed by the EU Commission fulfils the main requirements of an efficient scheme. However, with respect to transparency the EU Commission proposal can be improved. Side-payments received by member states that host a high number of refugees relative to their economic capacity should be funded by a rearrangement within the EU budget.

Whom to contact

For Researchers

Vice President Department Head

If you have any further questions please contact me.

+49 345 7753-800 Request per E-MailFor Journalists

Head of Public Relations

If you have any further questions please contact me.

+49 345 7753-720 Request per E-MailIWH list of experts

The IWH list of experts provides an overview of IWH research topics and the researchers and scientists in these areas. The relevant experts for the topics listed there can be reached for questions as usual through the IWH Press Office.