East Germany's lead over West Germany in terms of growth is bound to shrink – Implications of the Joint Economic Forecast Spring 2024 for the East German economy

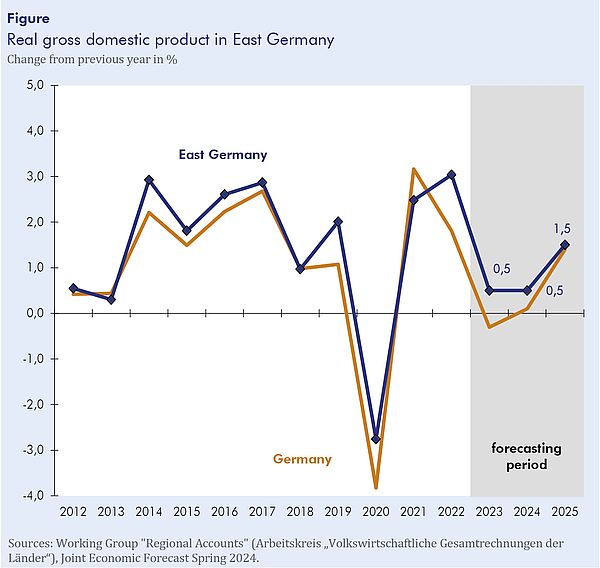

In its spring report, the Joint Economic Forecast states that the German economy is in a prolonged phase of weakness. A recovery is likely to start in spring, but the overall momentum will not be strong. Production in East Germany was probably somewhat more robust last year than in the west. This is because public and other service providers have a considerably greater weight here (just under 30%) than in West Germany (just under 20%), and these sectors of the economy expanded in 2023. In addition, private consumption has been supported by the increase in the minimum wage, which is frequently paid in East Germany. In addition, the statutory pension was increased by 5.9%, 1.5 percentage points more than in the west. Overall, production in East Germany will probably have increased by 0.5% in 2023 (see figure). “This means that the East German economy has been growing a bit faster than the economy in Germany as a whole for the past ten years, primarily due to higher momentum in the consumer-related sectors of trade, transport and hospitality, but also in manufacturing,” says Oliver Holtemöller, Head of the Department Macroeconomics and Vice President at the IWH.

East Germany is forecasted to growth by 0.5% in 2024, with Germany as a whole growing by 0.1%. “The narrowing gap in production momentum is partly due to barely increasing employment in East Germany, because the population is ageing rapidly,” says Holtemöller. In addition, from 2024 pensions will not increase stronger in the east because the equalisation of the pension value between east and west was achieved in 2023. However, unlike in the west, the manufacturing industry is likely to continue expanding, driven not least by the high subsidies for the semiconductor industry in Saxony and Saxony-Anhalt. For this reason, the rate of expansion in East Germany in 2025 is expected to remain, with 1.5%, slightly higher than in Germany as a whole (1.4%) despite the less favourable demographic trend.

Joint Economic Forecast, Spring 2024 Report (in German):

Joint Economic Forecast: Deutsche Wirtschaft kränkelt – Reform der Schuldenbremse kein Allheilmittel. Kiel, March 2024.

Whom to contact

For Researchers

Vice President Department Head

If you have any further questions please contact me.

+49 345 7753-800 Request per E-MailFor Journalists

Head of Public Relations

If you have any further questions please contact me.

+49 345 7753-720 Request per E-MailIWH list of experts

The IWH list of experts provides an overview of IWH research topics and the researchers and scientists in these areas. The relevant experts for the topics listed there can be reached for questions as usual through the IWH Press Office.

Related Publications

Deutsche Wirtschaft kränkelt – Reform der Schuldenbremse kein Allheilmittel

in: Dienstleistungsauftrag des Bundesministeriums für Wirtschaft und Klimaschutz, 1, 2024

Abstract

Die Wirtschaft in Deutschland ist angeschlagen. Eine bis zuletzt zähe konjunkturelle Schwächephase geht mit schwindenden Wachstumskräften einher. In der lahmenden gesamtwirtschaftlichen Entwicklung überlagern sich somit konjunkturelle und strukturelle Faktoren. Zwar dürfte ab dem Frühjahr eine Erholung einsetzen, die Dynamik wird aber insgesamt nicht allzu groß ausfallen. Zeitlich verzögert und in abgeschwächter Form hat das konjunkturelle Grundmuster, das die Institute im vergangenen Herbstgutachten gezeichnet hatten, im Prognosezeitraum weiterhin Bestand. Im laufenden Jahr avanciert der private Konsum zur wichtigsten Triebkraft für die Konjunktur. Nachdem der ab Mitte 2021 einsetzende Teuerungsschub die Massenkaufkraft zwei Jahre lang drastisch geschmälert hatte, steigen die real verfügbaren Einkommen nun wieder deutlich. Zum einen bildet sich der kräftige Preisauftrieb weiter zurück, zum anderen werden nun mehr und mehr höhere Lohnabschlüsse wirksam, die zunächst nur verzögert an die hohe Geldentwertung angepasst werden konnten. Zudem schlägt auch bei den monetären Sozialleistungen in beiden Prognosejahren wieder ein deutliches reales Plus zu Buche. Damit fließt insgesamt mehr Kaufkraft an private Haushalte. Während somit in diesem Jahr die konsumbezogenen Auftriebskräfte dominieren, trägt im kommenden Jahr vermehrt das Auslandsgeschäft die Konjunktur. Alles in allem revidieren die Institute ihre Prognose für die Veränderung des Bruttoinlandsprodukts im laufenden Jahr gegenüber ihrem Herbstgutachten deutlich um 1,2 Prozentpunkte nach unten auf nunmehr 0,1 %. Die Prognose für die Rate im kommenden Jahr bleibt mit 1,4 % nahezu unverändert (Rücknahme um 0,1 Prozentpunkte), geht aber mit einem um über 30 Mrd. Euro geringeren Volumen der Wirtschaftsleistung einher. Die Werte für die jahresdurchschnittliche Veränderung überzeichnen die Unterschiede in der konjunkturellen Dynamik beider Jahre, die ausweislich der jeweiligen Verlaufsraten mit 1,0 % und 1,5 % weniger ausgeprägt sind. Gleichwohl verlagert sich die Erholung nunmehr stärker in das kommende Jahr.