The downturn in 2023 is milder in East Germany than in Germany as a whole – Implications of the Joint Economic Forecast Autumn 2023 and of Länder data from recent publications of the Statistical Offices

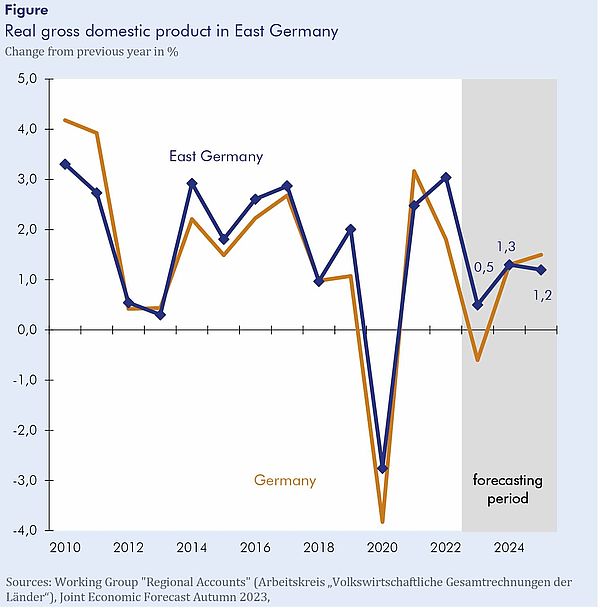

In its autumn report, the Joint Economic Forecast states that the German economy has been in a downturn for more than a year and will not gain strength before the end of 2023. In East Germany, however, economic activity has been somewhat stronger over the past four quarters: According to the Arbeitskreis “Volkswirtschaftliche Gesamtrechnungen der Länder”, East German GDP was 0.2% higher in the first half of 2023 than a year earlier, while it was 0.3% lower for Germany as a whole. Regional differences in manufacturing activity were strong: Gross domestic product in Saxony-Anhalt fell by 3.2%, most likely because the chemical industry in this federal state suffered from extreme increases in energy prices. By contrast, Brandenburg's gross domestic product was 6% higher than a year earlier. The key factor here was that the new large electric car factory in Grünheide step by step expanded production that started in March 2022. “Sales and orders received in the manufacturing sector in the first half of 2023 also point to somewhat higher momentum in East Germany”, says Oliver Holtemöller, Head of the Department Macroeconomics and Vice President at the IWH. “In addition, disposable incomes in East Germany have been growing more strongly than those in the west for several years”. East German real gross wages and salaries in 2022 were 19.5% above their 2015 level, while those in West Germany were only 16.1% higher. This year, incomes will be supported by a large increase in the minimum wage (to twelve euros per hour from October 2022), which is more frequently paid in the east. In addition, the statutory pension will increase by 5.9%, 1.5 percentage points more than in the west.

“In the coming years, however, East Germany's GDP is unlikely to expand at a faster rate than that of Germany as a whole, since the number of people in employment will fall for demographic reasons”, says Holtemöller. Employment subject to social security contributions in East Germany has hardly increased at all recently, in June by 0.3% compared with the same month a year earlier (Germany as a whole: 0.7%). In addition, there will be no higher pension increases in the east from 2024 onwards.

Overall, East German GDP is expected to grow by 0.5% in 2023, while output in Germany as a whole will fall by 0.6% (see figure). Next year, both expansion rates are likely to be 1.3%, and for 2025, East German output is forecast to grow by 1.2%, somewhat slower than in Germany as a whole (1.5%). This means that per capita GDP in East Germany will remain at around 80% of the level in West Germany. The East German unemployment rate as defined by the Federal Employment Agency will be 7.1% in 2022 and 7.0% next year, falling to 6.7% in 2024.

Joint Economic Forecast, Autumn 2023 Report (in German):

Joint Economic Forecast: Kaufkraft kehrt zurück – Politische Unsicherheit hoch. Halle (Saale), September 2023.

Whom to contact

For Researchers

Vice President Department Head

If you have any further questions please contact me.

+49 345 7753-800 Request per E-MailFor Journalists

Head of Public Relations

If you have any further questions please contact me.

+49 345 7753-720 Request per E-MailIWH list of experts

The IWH list of experts provides an overview of IWH research topics and the researchers and scientists in these areas. The relevant experts for the topics listed there can be reached for questions as usual through the IWH Press Office.

Related Publications

Gemeinschaftsdiagnose: Kaufkraft kehrt zurück – Politische Unsicherheit hoch

in: Dienstleistungsauftrag des Bundesministeriums für Wirtschaft und Klimaschutz, 2, 2023

Abstract

Deutschland befindet sich seit über einem Jahr im Abschwung. Der sprunghafte Anstieg der Energiepreise im Jahr 2022 hat der Erholung von der Pandemie ein jähes Ende bereitet. Die schon zuvor anziehende Verbraucherpreisinflation ist zwischenzeitlich auf über 8% gestiegen. Dadurch wird den privaten Haushalten Kaufkraft entzogen. Die Leitzinsen sind um über vier Prozentpunkte gestiegen. Das trifft insbesondere die Bauwirtschaft. <br /><br /> Die Stimmung in den Unternehmen hat sich zuletzt erneut verschlechtert, dazu trägt auch politische Unsicherheit bei. Insgesamt deuten die Indikatoren darauf hin, dass die Produktion im dritten Quartal 2023 nochmals spürbar gesunken ist. Allerdings haben mittlerweile die Löhne aufgrund der Teuerung angezogen, die Energiepreise abgenommen und die Exporteure die höheren Kosten teilweise weitergegeben, sodass Kaufkraft zurückkehrt. Daher dürfte der Abschwung zum Jahresende abklingen und der Auslastungsgrad der Wirtschaft im weiteren Verlauf wieder steigen.<br /><br /> Alles in allem wird das Bruttoinlandsprodukt im Jahr 2023 um 0,6% sinken. Damit revidieren die Institute ihre Prognose vom Frühjahr 2023 kräftig um 0,9 Prozentpunkte nach unten. Der wichtigste Grund dafür ist, dass sich die Industrie und der Konsum langsamer erholen als im Frühjahr prognostiziert worden war. Für das Jahr 2024 liegt die Prognose mit 1,3% nur 0,2 Prozentpunkte unter der aus dem Frühjahr. Danach wird sich bemerkbar machen, dass das Potenzialwachstum aufgrund der schrumpfenden Erwerbsbevölkerung mittelfristig deutlich zusammenschmilzt.