From Pandemic to Energy Crisis: Economy and Politics under Permanent Stress

"The recovery process in the German economy is once again being delayed. The economic picture is shaped by opposing forces, all of which are driving up prices," says Stefan Kooths, vice president and research director business cycles and growth at the Kiel Institute for the World Economy.

"Fading pandemic restrictions are supporting the service sectors while continuing supply chain bottlenecks in the wake of the COVID-19 crisis are still disturbing manufacturing output. The shockwaves from the war in Ukraine are weighing on economic activity on both the supply side and the demand side. Government stimulus packages during the pandemic already had an inflationary effect. Increasing prices of critical energy commodities following the Russian invasion further fuel the upward pressure on prices."

Due to the high level of uncertainty about energy supplies from Russia, which are important for Germany’s economic performance, the institutes have calculated two scenarios in their spring report. One assumes ongoing gas deliveries and no further economic escalation from the war in Ukraine (baseline scenario), one assumes a sudden supply stop of Russian energy (adverse scenario).

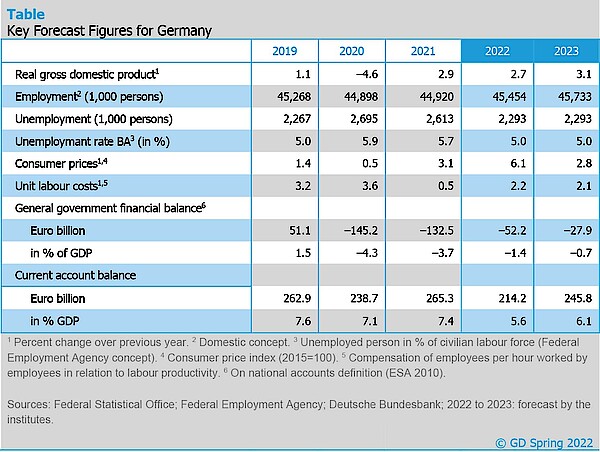

In the baseline scenario, Germany's gross domestic product (GDP) increases by 2.7% in 2022, and in the event of an energy supply stop by only 1.9%. In their fall report, the institutes’ forecast was 4.8%. The main reasons for the revision are the war in Ukraine and the worse than expected course of the pandemic in the past winter half-year. In 2023, GDP is forecast to increase by 3.1%, and to contract by 2.2% in the event of a supply stop (Autumn report +1.9%). The cumulative loss of GDP in 2022 and 2023 in the event of a supply freeze is likely to be around 220 billion euros, equivalent to more than 6.5% of annual economic output.

The inflation forecast amounts to 6.1% in 2022, the highest number in 40 years. In the event of an energy supply stop, it would even increase to 7.3%, a record-high in post-war Germany. Next year's rate of 2.8% (supply stop: 5%) will also remain well above the average since reunification.

According to the baseline scenario, the unemployment rate will fall from 5.7% in the previous year to 5.0% (2022 and 2023). The adverse scenario foresees 5.2% (2022) and 6.0% (2023) with most of the shock being absorbed by reduced working hours.

The public deficit is expected to narrow significantly as pandemic fiscal support expires, government revenues rise in the wake of the upswing and extra funds for climate protection and defense are likely to be drained off only slowly. According to the forecast, the deficit will fall to 52.2 billion euros in the current year and to 27.9 billion euros in the coming year. In case of a gas supply stop a deficit of just over 76 billion euros is expected in 2022 (2.0% of GDP), and of about 160 billion euros in 2023 (4.1% of GDP).

"If gas supplies were to be cut off, the German economy would undergo a sharp recession. In terms of economic policy, it would then be important to support marketable production structures without halting structural change. This change will accelerate for gas-intensive industries even without a boycott, as dependence on Russian supplies, which have been available at favorable prices up to now, is to be overcome quickly anyway," Kooths said. "Policymakers should be careful not to provide poorly targeted transfers to cushion high energy prices. If such support schemes are handed out on a wide front, it will further drive up inflation and undermine the important signaling effect of higher energy prices. This in turn exacerbates the problems of low-income households and increases overall economic costs.”

The Joint Economic Forecast was prepared by the German Institute for Economic Research (DIW Berlin), the ifo Institute (Munich), the Kiel Institute for the World Economy (IfW Kiel), the Halle Institute for Economic Research (IWH), and RWI (Essen).

The full report is available here: www.gemeinschaftsdiagnose.de/category/gutachten/.

About the Joint Economic Forecast

The Joint Economic Forecast is published twice a year on behalf of the German Federal Ministry for Economic Affairs and Climate Action. The following institutes participated in the spring report 2022:

- German Institute for Economic Research (DIW Berlin)

- ifo Institute – Leibniz Institute for Economic Research at the University of Munich in cooperation with the KOF Swiss Economic Institute at ETH Zurich

- Kiel Institute for the World Economy (IfW Kiel)

- Halle Institute for Economic Research (IWH) – Member of the Leibniz Association

- RWI – Leibniz Institute for Economic Research in cooperation with the Institute for Advanced Studies Vienna

Scientific Contacts

Professor Dr Stefan Kooths

Kiel Institute for the World Economy (IfW Kiel)

Phone +49 431 8814 579 or +49 30 2067 9664

Stefan.Kooths@ifw-kiel.de

Professor Dr Martin Gornig

German Institute for Economic Research (DIW Berlin)

Phone +49 30 89789 352

Mgornig@diw.de

Professor Dr Timo Wollmershäuser

ifo Institute – Leibniz Institute for Economic Research at the University of Munich

Phone +49 89 9224 1406

Wollmershaeuser@ifo.de

Professor Dr Oliver Holtemöller

Halle Institute for Economic Research (IWH) – Member of the Leibniz Association

Phone +49 345 7753 800

Oliver.Holtemoeller@iwh-halle.de

Professor Dr Torsten Schmidt

RWI – Leibniz Institute for Economic Research

Phone +49 201 8149 287

Torsten.Schmidt@rwi-essen.de

Whom to contact

For Researchers

Vice President Department Head

If you have any further questions please contact me.

+49 345 7753-800 Request per E-MailFor Journalists

Internal and External Communications

If you have any further questions please contact me.

+49 345 7753-832 Request per E-MailIWH list of experts

The IWH list of experts provides an overview of IWH research topics and the researchers and scientists in these areas. The relevant experts for the topics listed there can be reached for questions as usual through the IWH Press Office.

Related Publications

Von der Pandemie zur Energiekrise – Wirtschaft und Politik im Dauerstress

in: Dienstleistungsauftrag des Bundesministeriums für Wirtschaft und Klimaschutz, 1, 2022

Abstract

Die deutsche Wirtschaft steuert durch schwieriges Fahrwasser. Die Auftriebskräfte durch den Wegfall der Pandemiebeschränkungen, die Nachwehen der Corona-Krise und die Schockwellen durch den Krieg in der Ukraine sorgen für gegenläufige konjunkturelle Strömungen. Allen Einflüssen gemeinsam ist ihre preistreibende Wirkung. Im zurückliegenden Winterhalbjahr haben vor allem die Maßnahmen zum Infektionsschutz die Wirtschaftsleistung gedämpft. Unter der Voraussetzung, dass das Kriegsgeschehen in der Ukraine mit Blick auf die ökonomische Aktivität nicht weiter eskaliert, werden die konjunkturellen Auftriebskräfte ab dem Frühjahr die Oberhand gewinnen. Nach einem schwachen Jahresauftakt dürfte das Bruttoinlandsprodukt im zweiten Quartal zwar deutlich zulegen, ohne die Belastung durch den Krieg in der Ukraine würde das Plus aber kräftiger ausfallen. Insgesamt verzögert sich damit der Erholungsprozess abermals. Das Vorkrisenniveau der Wirschaftsleistung wird demnach erst im dritten Quartal des laufenden Jahres erreicht werden. Alles in allem erwarten die Institute einen Anstieg des Bruttoinlandsproduktes von 2,7% für dieses Jahr und 3,1% für nächstes Jahr. Im kommenden Jahr driftet die deutsche Wirtschaft in eine leichte Überauslastung. Maßgeblich dafür sind der hohe Auftragsüberhang in der Industrie sowie nachholende Konsumaktivität. Im Falle eines sofortigen Embargos für die Öl- und Gaslieferungen aus Russland in die Europäische Union würde hingegen die deutsche Wirtschaft in eine scharfe Rezession geraten. Der kumulierte Verlust an gesamtwirtschaftlicher Produktion dürfte sich in diesem Fall bereits in den beiden Jahren 2022 und 2023 auf rund 220 Mrd. Euro belaufen, was mehr als 6,5% der jährlichen Wirschaftsleistung entspricht.