Pandemic delays upswing – Demography slows growth

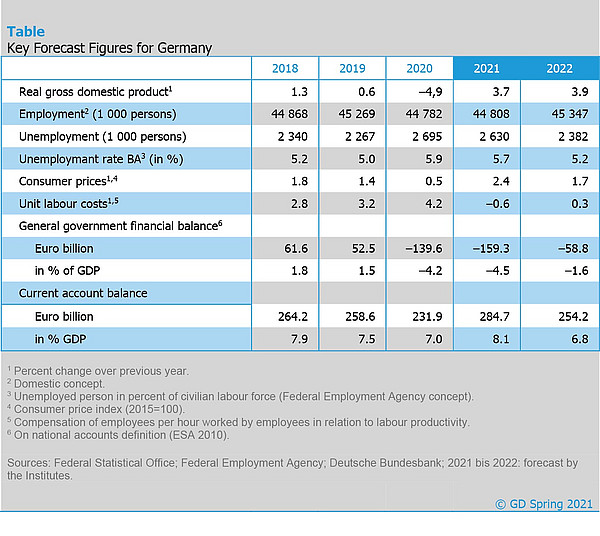

"Economic output is likely to have dropped by 1.8% in the first quarter due to the continuing shutdown," said Torsten Schmidt, Chief Economist at RWI – Leibniz Institute for Economic Research. The new wave of infections and the associated containment measures lead to the downward revision of the forecast for 2021 by 1 percentage point compared to the fall forecast 2020.

In their forecast, the institutes assume that the current shutdown will continue for the time being and that the most recent easing measures will be largely reversed. Further easing is not expected until the middle of the second quarter, with restrictions probably lifted by the end of the third quarter. "We expect a vigorous expansion of economic activities as the measures are gradually lifted over the course of the six months through the summer, especially in the services sector that was particularly affected by the pandemic," Schmidt added.

Employment is also likely to gain momentum in view of the expected easing of restrictions. On average, employment is expected to rise by 26,000 over 2021. The rise is estimated at 539,000 over the coming year, with precrisis levels being reached in the first half-year. Unemployment levels are also expected to drop more sharply as the infection control measures are gradually lifted.

Public budgets are expected to show a deficit of 159 billion euros in 2021, slightly higher than in the previous year. Tax revenues are already rising again due to the economic situation. However, spending on vaccinations and tests is causing social benefits in kind to rise sharply. Moreover, government investment is likely to continue expanding, especially due to the funds available in investment programmes. In relation to GDP, the general government budget deficit is expected to remain roughly the same at 4.5% in 2021 and to drop significantly to 1.6% in 2022.

The coronavirus pandemic is leaving its mark on production potential as well. Current forecasts suggest that between 2020 and 2024, it is likely to be on average around 1.1% below the levels originally estimated prior to the Corona crisis. In addition, there are already signs that Germany is facing a far-reaching demographic transition in the years ahead. The total workforce will shrink as the baby boomers reach retirement age, accompanied by a sharp rise in the proportion of older people. This will have serious consequences for growth potential: Projections indicate that the rate of growth potential is expected to decline by around one percentage point by 2030.

The further development of the pandemic remains the most significant downside risk to the outlook. Bottlenecks and delays may still occur in the delivery of vaccines and tests. Moreover, the emergence of new virus mutations might erode the effectiveness of vaccines, potentially halting the opening process and once again causing setbacks in the economic recovery.

The Joint Economic Forecast was prepared by the DIW (Berlin), the ifo Institute (Munich), the IfW (Kiel), the IWH (Halle), and the RWI (Essen).

Complete report (in German)

Joint Economic Forecast Project Group: Pandemic delays upswing – Demography slows growth. Spring 2021. Essen 2021.

The complete version of the report (in German language) will be available on the IWH website and at www.gemeinschaftsdiagnose.de/category/gutachten/.

About the Joint Economic Forecast

The Joint Economic Forecast is published twice a year on behalf of the German Federal Ministry for Economic Affairs and Energy. The following institutes participated in the spring report 2021:

- German Institute for Economic Research (DIW Berlin)

- ifo Institute – Leibniz Institute for Economic Research at the University of Munich

in cooperation with the KOF Swiss Economic Institute at ETH Zurich - Kiel Institute for the World Economy (IfW Kiel)

- Halle Institute for Economic Research (IWH) – Member of the Leibniz Association

- RWI – Leibniz Institute for Economic Research in cooperation with the Institute for Advanced Studies Vienna

Scientific Contacts

Dr. Claus Michelsen

German Institute for Economic Research (DIW Berlin)

Tel +49 30 89789 458

CMichelsen@diw.de

Professor Dr. Timo Wollmershäuser

ifo Institute – Leibniz Institute for Economic Research at the University of Munich

Tel +49 89 9224 1406

Wollmershaeuser@ifo.de

Professor Dr. Stefan Kooths

Kiel Institute for the World Economy (IfW Kiel)

Tel +49 431 8814 579 oder +49 30 2067 9664

Stefan.Kooths@ifw-kiel.de

Professor Dr. Oliver Holtemöller

Halle Institute for Economic Research (IWH) – Member of the Leibniz Association

Tel +49 345 7753 800

Oliver.Holtemoeller@iwh-halle.de

Professor Dr. Torsten Schmidt

RWI – Leibniz Institute for Economic Research

Tel +49 201 8149 287

Torsten.Schmidt@rwi-essen.de

Whom to contact

For Researchers

Vice President Department Head

If you have any further questions please contact me.

+49 345 7753-800 Request per E-MailFor Journalists

Internal and External Communications

If you have any further questions please contact me.

+49 345 7753-832 Request per E-MailIWH list of experts

The IWH list of experts provides an overview of IWH research topics and the researchers and scientists in these areas. The relevant experts for the topics listed there can be reached for questions as usual through the IWH Press Office.

Related Publications

Pandemie verzögert Aufschwung – Demografie bremst Wachstum

in: Dienstleistungsauftrag des Bundesministeriums für Wirtschaft und Energie, 1, 2021

Abstract

Das erste Jahr der Corona-Pandemie stand in Deutschland im Zeichen extremer Schwankungen der ökonomischen Aktivität und einer massiven Lähmung der Binnenwirtschaft. Der kräftige Erholungsprozess nach dem Ende des Shutdowns im vergangenen Frühjahr kam im Zuge der zweiten Infektionswelle über das zurückliegende Winterhalbjahr insgesamt zum Erliegen, wobei es große Unterschiede zwischen Industrie und Dienstleistern gibt. Angesichts des aktuellen Infektionsgeschehens gehen die Institute davon aus, dass der derzeitige Shutdown zunächst fortgesetzt wird und die zuletzt erfolgten Lockerungen wieder weitgehend zurückgenommen werden. Erst ab Mitte des zweiten Quartals setzen Lockerungsschritte ein, die es den im Shutdown befindlichen Unternehmen erlauben, ihre Aktivitäten nach und nach wieder aufzunehmen. Bis zum Ende des dritten Quartals sollten dann alle Beschränkungen aufgehoben worden sein, weil bis dahin insbesondere mit einem weitreichenden Impffortschritt zu rechnen ist. Insgesamt dürfte das Bruttoinlandsprodukt in diesem Jahr um 3,7% zulegen. Die deutliche Erholung im zweiten Halbjahr 2021 wirkt sich auch erheblich auf die Jahresdurchschnittsrate für das Jahr 2022 aus, die nach vorliegender Prognose 3,9% beträgt.