Stubborn Core Inflation – Time for Supply Side Policies

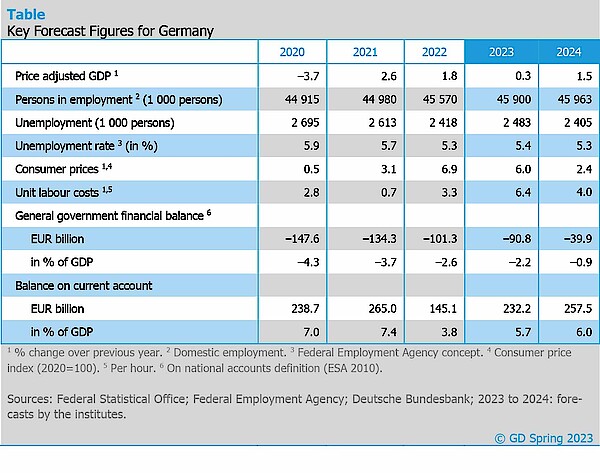

Government relief measures and foreseeably high wage increases in Germany are strengthening domestic demand and keeping domestic inflation high. Only next year will this aspect of inflationary pressure also ease, bringing the inflation rate down noticeably to 2.4%. Gross domestic product is then expected to grow more strongly again by 1.5%.

There is good news for the labour market: The number of people in employment is likely to increase again, from 45.6 million in 2022 to 45.9 million in 2023 and 46.0 million in 2024. This year, the number of unemployed will rise temporarily from 2.42 million to 2.48 million as it will take Ukrainian refugees a little time to enter the labour market. In the coming year, however, unemployment is expected to fall again to 2.41 million people.

The government will reduce its deficit only slightly to 2.2% of nominal GDP in the current year, since fiscal policy will remain expansionary for the time being. Only next year will policy be tightened more significantly, bringing the deficit down to 0.9%. A large share of the previous year’s terms-of-trade losses, which measure the loss of purchasing power in the overall economy due to the sharp rise in the price of energy imports, will be recovered by the end of 2024. As a result, the current account balance will rise again to 6.0% of economic output, after temporarily falling to 3.8% last year.

Full-length version of the report (German):

Projektgruppe Gemeinschaftsdiagnose: Inflation im Kern hoch – Angebotskräfte jetzt stärken. Frühjahr 2023. Munich 2023.

The full-length version of the report is available here:

About the Joint Economic Forecast

The Joint Economic Forecast is published twice a year on behalf of the Federal Ministry for Economic Affairs and Climate Action. The following institutes participated in the spring report 2023:

- ifo Institute – Leibniz Institute for Economic Research at the University of Munich in cooperation with the Austrian Institute of Economic Research (WIFO) Vienna

- Kiel Institute for the World Economy (IfW Kiel)

- Halle Institute for Economic Research (IWH) – Member of the Leibniz Association

- RWI – Leibniz Institute for Economic Research in cooperation with the Institute for Advanced Studies Vienna

Scientific Contacts

Professor Dr Timo Wollmershäuser

ifo Institute – Leibniz Institute for Economic Research at the University of Munich

Phone +49 89 9224 1406

Wollmershaeuser@ifo.de

Professor Dr Stefan Kooths

Kiel Institute for the World Economy (IfW Kiel)

Phone +49 431 8814 579 or +49 30 2067 9664

Stefan.Kooths@ifw-kiel.de

Professor Dr Oliver Holtemöller

Halle Institute for Economic Research (IWH) – Member of the Leibniz Association

Phone +49 345 7753 800

Oliver.Holtemoeller@iwh-halle.de

Professor Dr Torsten Schmidt

RWI – Leibniz Institute for Economic Research

Phone +49 201 8149 287

Torsten.Schmidt@rwi-essen.de

Whom to contact

For Researchers

Vice President Department Head

If you have any further questions please contact me.

+49 345 7753-800 Request per E-MailFor Journalists

Internal and External Communications

If you have any further questions please contact me.

+49 345 7753-832 Request per E-MailIWH list of experts

The IWH list of experts provides an overview of IWH research topics and the researchers and scientists in these areas. The relevant experts for the topics listed there can be reached for questions as usual through the IWH Press Office.

Related Publications

Gemeinschaftsdiagnose: Inflation im Kern hoch – Angebotskräfte jetzt stärken

in: Dienstleistungsauftrag des Bundesministeriums für Wirtschaft und Klimaschutz, 1, 2023

Abstract

<p>Der konjunkturelle Rückschlag im Winterhalbjahr 2022/2023 dürfte glimpflicher ausgefallen sein als im Herbst befürchtet. Die angebotsseitigen Störungen, die die deutsche Wirtschaft seit geraumer Zeit belasten, haben nachgelassen. Ein merklicher Rückgang der Inflationsraten wird jedoch noch etwas auf sich warten lassen, da der Nachfragesog vorerst kaum geringer werden dürfte. Dazu tragen neben den staatlichen Entlastungsmaßnahmen auch die absehbar hohen Lohnsteigerungen bei. Die Inflationsrate wird im Jahr 2023 mit 6,0% nur wenig niedriger liegen als im Vorjahr. Erst im kommenden Jahr dürfte die Rate, insbesondere aufgrund der rückläufigen Energiepreise, spürbar sinken. Der Rückgang der Kerninflationsrate (also der Anstieg der Verbraucherpreise ohne Energie) fällt zunächst deutlich schwächer aus. Sie dürfte von 6,2% im laufenden Jahr nur langsam auf 3,3% im kommenden Jahr zurückgehen. <br /><br />Das Verarbeitende Gewerbe wird in den kommenden Quartalen zur Konjunkturstütze werden, da es unmittelbar vom Abflauen der Lieferengpässe und der wieder etwas günstigeren Energie profitiert. Da die Reallöhne wieder anziehen, wird auch der private Konsum im weiteren Verlauf zur gesamtwirtschaftlichen Expansion beitragen. Die Bauwirtschaft wird die Konjunktur hingegen bremsen, da die Nachfrage auch als Folge der gestiegenen Finanzierungskosten schwach bleiben wird. Das preisbereinigte Bruttoinlandsprodukt wird in diesem Jahr um 0,3% und im kommenden Jahr um 1,5% zulegen. Damit heben die Institute ihre Prognose vom Herbst 2022 für das laufende Jahr spürbar um 0,7 Prozentpunkte an, während die Prognose für das kommende Jahr um 0,4 Prozentpunkte gesenkt wird. Die Wirtschaftspolitik hat in den vergangenen Jahren die angebotspolitischen Zügel weitgehend schleifen lassen, auch in Zeiten, in denen kein akutes Krisenmanagement anstand. Umso größer ist nun der Reformbedarf, um insbesondere die Herausforderungen des demografischen Wandels und der Energiewende zu bewältigen. Beide erfordern potenzialstärkende Maßnahmen, auch um die sich verschärfenden Verteilungskonflikte einzuhegen. </p>